The bit of British genius you’re holding in your hand

The bit of British genius you’re holding in your hand

Ask anyone if Britain makes mobile phones, and the answer would be a resounding no. Most would name Apple, Samsung or Xiaomi – the smartphone giants of America, South Korea and China, respectively.

It's true that there are no big mobile phone makers here. But no one would think that in their hands, they also hold a little piece of British tech genius — a chip designed by Cambridge firm, Arm Holdings.

The firm is a giant in semiconductor design and one of our country's modern-day tech triumphs, powering nearly 90% of the world's smartphones.

But in the labyrinth of semiconductor supply chains, Arm is the UK’s only real global player. Why?

Semiconductors are the building blocks of technology today. What bricks are to buildings, semiconductors are to smartphones, computers, and even military hardware. In 2022 China spent more on chips ($415.6 billion) than it did on crude oil imports ($365.7 billion). The most advanced chips play a central role in the global AI race, driving the AI models that run programmes such as ChatGPT.

Yet semiconductor supply chains are fraught with bottlenecks. Taiwanese chips support over a third of the world’s new computing power each year. Two Korean firms produce almost half of all memory chips. One Dutch company is the sole supplier of the machines that make cutting-edge chips.1

Semiconductors power Britain’s economy and military, and are crucial to leadership in other frontier technologies, so we need to manage this dynamic carefully – limiting our vulnerability to foreign actors and expanding domestic industries to get a slice of the future market.

It’s the same as we’ve argued before on other frontier technologies: when it comes to semiconductors, Britain can’t lead on everything. We should focus on the niches where we can realistically build an edge – chip design, and next-generation chips such as compound semiconductors – invest in public goods, and get Government out of the way to unlock private enterprise.

Not so fab

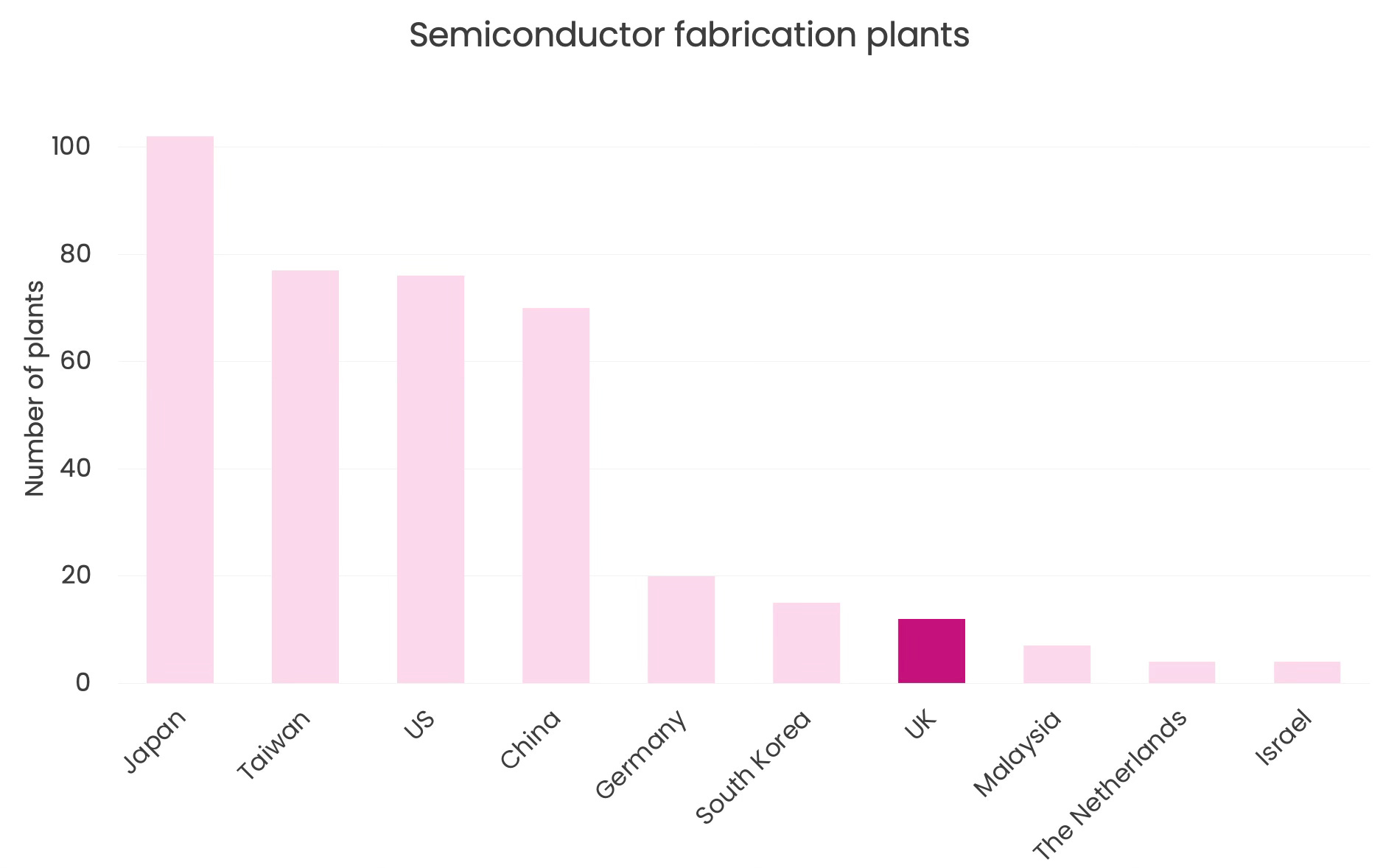

Anyone arguing that the UK should try to compete in advanced chip manufacturing is misguided. The chances of catching chip manufacturing leaders such as Taiwan and South Korea are nigh-on impossible. We have no large-scale cutting-edge silicon chip manufacturing facilities (known as ‘fabs’). Even with its less advanced facilities, the UK has eight times fewer than Japan, six times fewer than Taiwan and America, and just over half as many as Germany.

As Manchester University Professor Richard Jones puts it, “the only way it could happen is if one of the three companies at the frontier – Samsung, Intel or Taiwan Semiconductor Manufacturing Company (TSMC) – could be enticed to establish a manufacturing plant in the UK.”

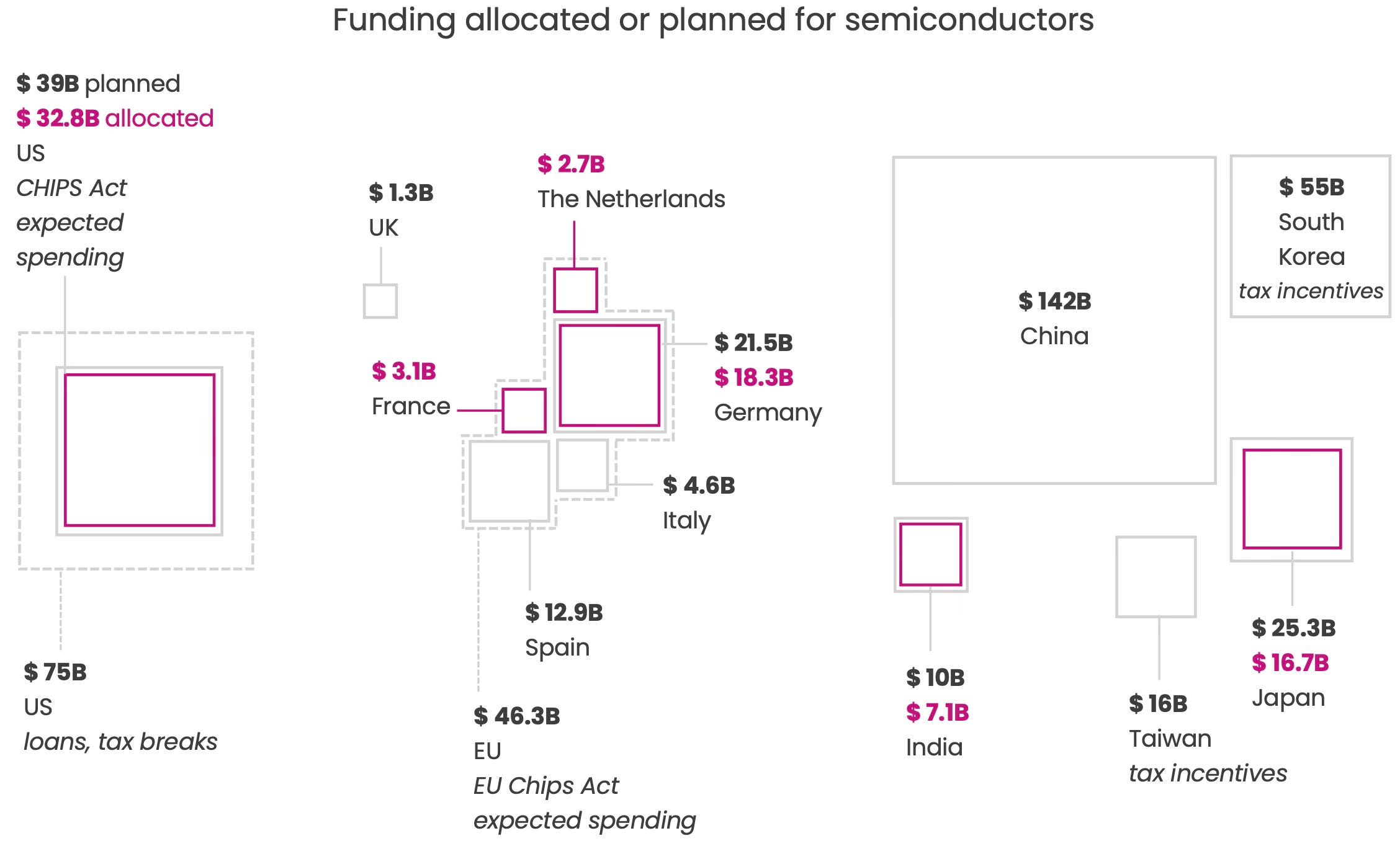

But enticing the big players to the UK would require huge sums of public funding. The US CHIPS Act handed out $39 billion in manufacturing subsidies. American taxpayers are paying over $6 billion to one Taiwanese company, TSMC, to build an advanced chip plant in Arizona. Germany is paying the same firm up to €5 billion to build a chip factory in Dresden. That’s five times Britain’s entire ten-year funding package for semiconductors.

The EU hopes to catch up, with the European Chips Act investing €43 billion from the public purse and leveraged private investments. But even this is likely too little too late to achieve the EU’s goal of doubling its market share in global chip manufacturing.

We need to be realistic about what’s possible. The UK’s share in the global semiconductor market is minor – we make around 0.25% of the world’s integrated circuit exports, none at the cutting-edge, just over 1% in chip-making equipment and about 1.5% in chemicals and materials.

Thankfully, the Government’s National Semiconductor Strategy reflects this reality. It says that manufacturing the most advanced chips is not achievable, and instead argues we should lead in chip design and IP, packaging, compound semiconductors and R&D.

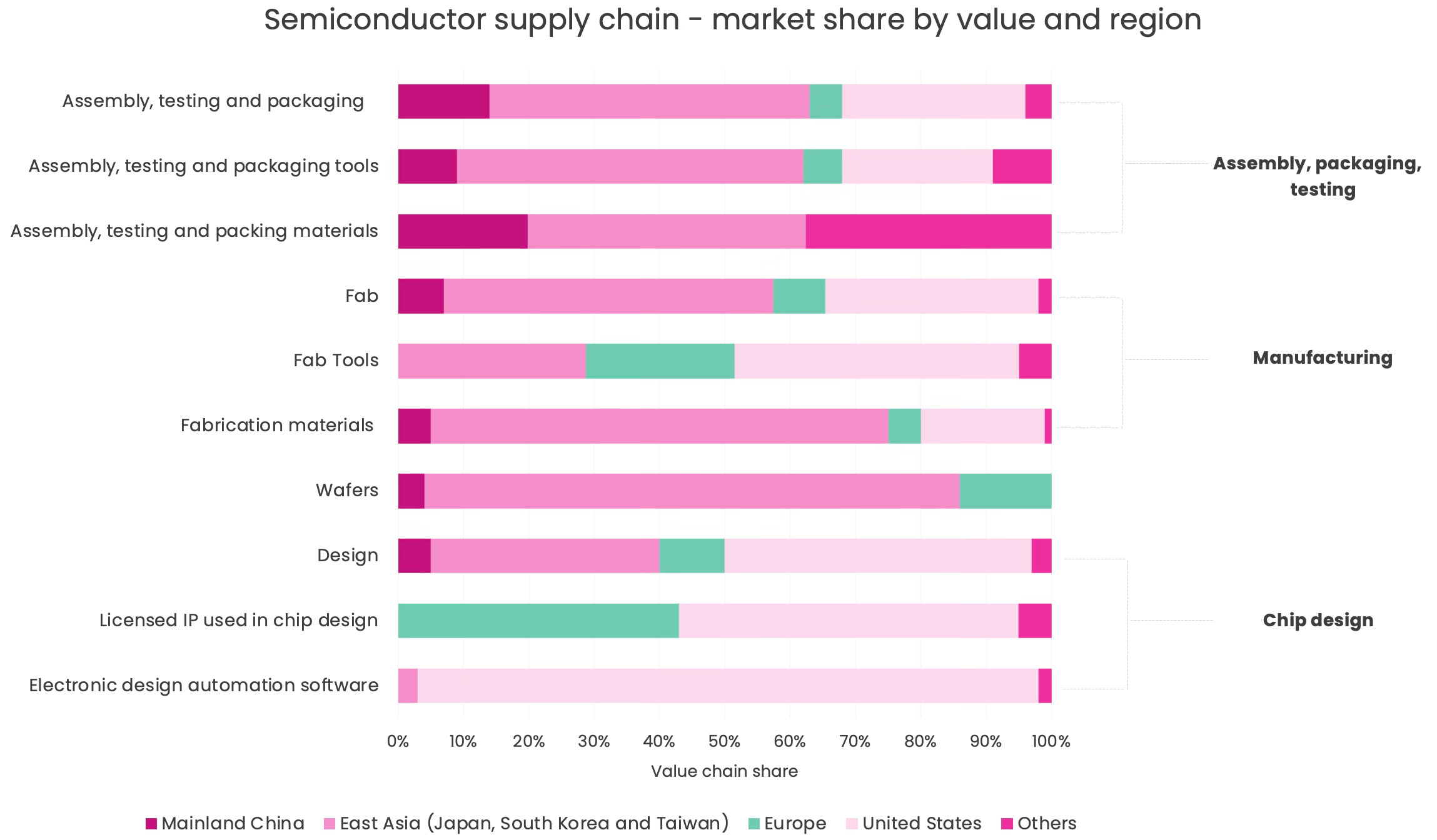

But even this narrowed list isn’t focused enough. Chip packaging is a distinct part of the chip-making process, where chips are enclosed in a protective case, which provides it with connections to other components and systems. In this global market, Europe as a whole barely registers, squeezed by the East Asian giants and the US to just 5% of market share.

Grand designs

Chip design is a better bet. This is the process of creating the architecture, components, and layout to perform specific electronic functions – similar to what Arm has come to pioneer. It’s lucrative, estimated to account for around a third of the global semiconductor value chain.

The UK has strengths in chip design. It has more than 100 companies focused on it, and is home to key chip design offices of global tech giants such as Apple and Intel.

Chip design will continue to be vital in the years to come too. Innovations in smaller, highly-specialised chips, that often use novel, non-silicon materials, are growing in importance. More and more technological companies are venturing into the chip design business.

We need more compound (chip) interest

Britain should apply its design strength to build a niche in next-generation chips, key among them are compound semiconductors. Silicon-based chips may make up four in every five chips today, but the compound chip market is expected to grow more than five-fold to $350 billion by 2030.

Compounds are in demand. We’ll need more and more of them for 5G communications and electric vehicles. Other frontier technologies will need them. Quantum will use compound semiconductors to create precise lasers. They could also be used for energy-efficient AI accelerator chips.

Britain’s market share in compounds has grown to $11 billion – around 8% of the global total. It has a compound semiconductor cluster in South Wales and Bristol, generating £500 million annually, employing over two thousand people, and contributing 2.5% of Welsh exports.

Chipping away at the frontier

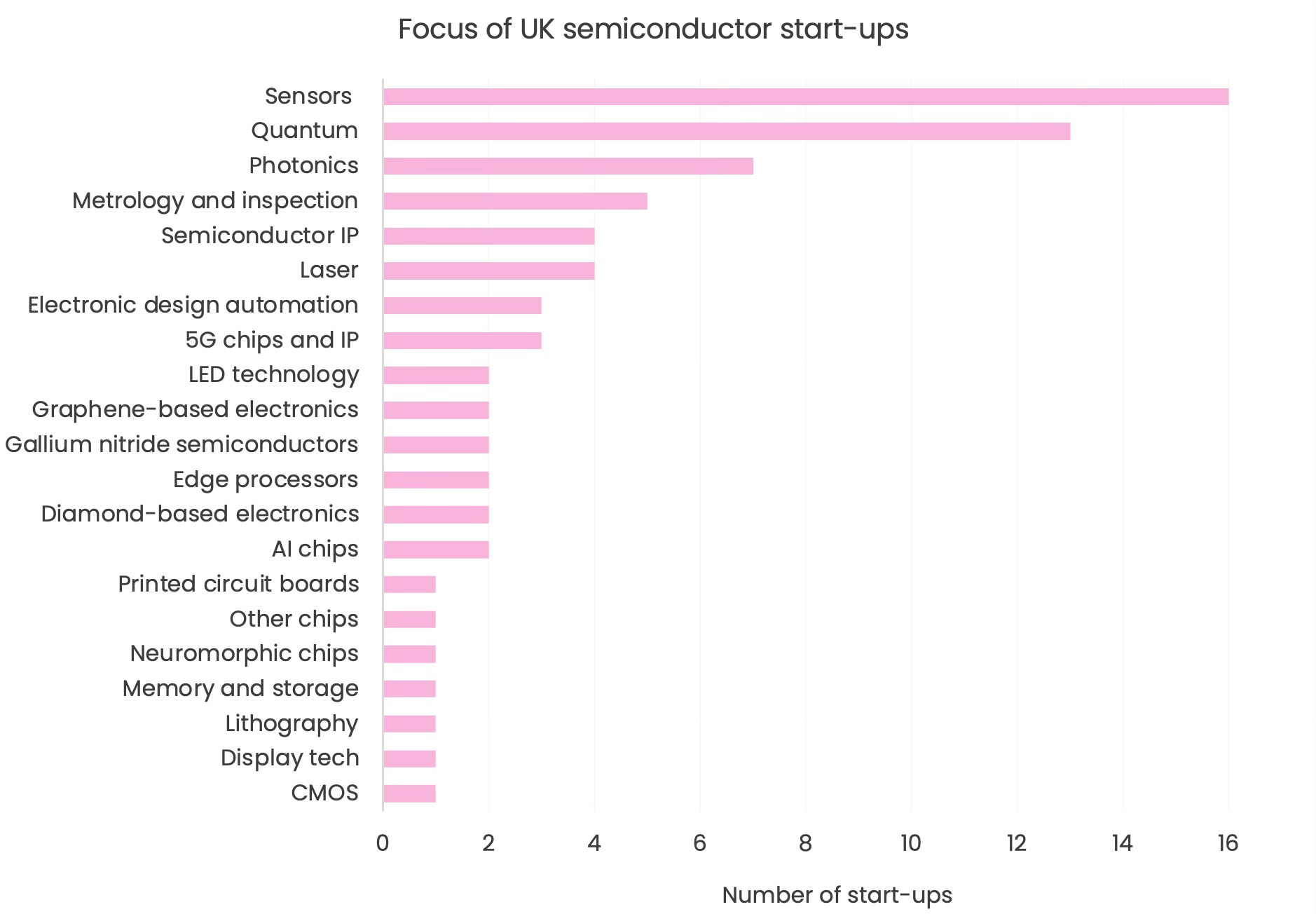

Compound semiconductors are just one form of next-gen chips – there are others, and there could be many more. British chip start-ups are at the forefront in many of these developments, particularly ones focused on driving advancements in quantum and photonics. Growth in these next-gen chips could lead to the UK gaining a competitive edge in quantum technologies too.

With strong semiconductor R&D capabilities, and startups focused on a wide range of areas, the UK should be setting its sights on taking a significant market share in next-gen chips, pioneering new forms of chips that can help drive its leadership in other frontier technologies such as quantum computers and advanced AI.

How to achieve this? Just this week the Government announced a new UK Semiconductor Institute to be “a single point of contact to promote the sector to investors and attract foreign investment.” But details so far are scant – particularly on funding, where it has only clarified where £30 million of its £1 billion semiconductor budget will go.2

Central to the Institute’s plan should be the creation of a new Advanced Semiconductor Research Fund focused on next-gen chip R&D and design. The fund should consist of three missions, each backed by up to £100 million from the Government’s semiconductor budget. These could include:

Quantum chips to enable scaling – a technical hurdle in quantum computing

Energy efficient AI accelerator chips

Compound semiconductors, optimised for electric vehicles

Each award should also include Government-funded test runs of prototypes with TSMC, similar to the Government-backed chip start-up incubator.

In the face of intense international competition, the UK cannot rely on the benevolence of others. Doubling down on areas of leadership will not only allow Britain to build prosperity through dominating niches in the value chain, but will give it leverageable strengths to boost UK security and resilience too.

What’s next…

Next we’ll be looking at the final technology of this series, future telecoms, and answering the question: Is 6G really all it's cracked up to be?

Chris Miller (2022) Chip War: The Fight for the World’s Most Critical Technology

£22 million for two Innovation and Knowledge Centres focused on skills, further £4.8 million for 11 semiconductor skills projects, and a £1.3 million incubator programme for chip start-ups.

| A guest post by

|

| A guest post by |